- Extra Space Storage Inc. recently reported third quarter 2025 earnings, showing year-over-year increases in sales and revenue but a decrease in net income and earnings per share.

- The company also updated its full-year guidance, narrowing its expectations for same-store revenue and NOI growth, and provided revised profit forecasts.

- Next, we’ll examine how Extra Space Storage’s cautious outlook for same-store revenue growth influences the company’s overall investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Extra Space Storage Investment Narrative Recap

To own Extra Space Storage, you have to believe in the resilience of its self-storage business model, which rests on steady occupancy, disciplined fee-based growth, and limited new supply. The latest quarterly update, showing positive year-over-year revenue but weaker net income, does not materially shift the short-term catalyst of revenue stabilization and margin recovery, while the biggest risk continues to be sluggish same-store sales amid a competitive market and tax cost pressures.

The updated full-year guidance, which now expects same-store revenue growth between -0.25% and +0.25%, directly highlights the challenge of reigniting top-line momentum. This subtle tightening of expectations signals management’s view that while some headwinds have moderated, the path to meaningful improvement in rental rates or occupancy remains slow and uncertain.

However, investors should be aware that in contrast to the company’s cautious guidance, there is still the risk that persistent property tax increases could structurally pressure margins if costs do not normalize as expected…

Read the full narrative on Extra Space Storage (it’s free!)

Extra Space Storage is projected to have $3.3 billion in revenue and $1.1 billion in earnings by 2028. This outlook assumes a yearly revenue decline of 1.3% and an earnings increase of about $125 million from the current earnings of $974.7 million.

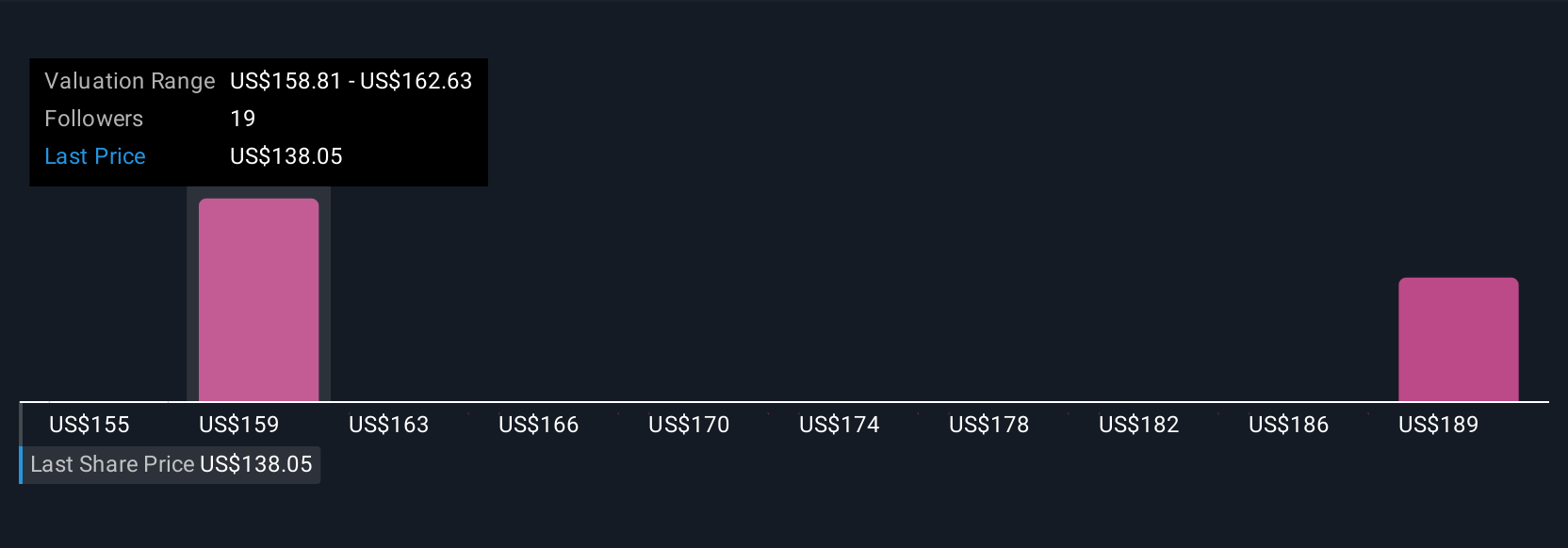

Uncover how Extra Space Storage’s forecasts yield a $157.75 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Fair value opinions from the Simply Wall St Community span from US$155 to nearly US$175 across 3 analyses, before factoring in the latest developments. While many focus on the company’s slow same-store revenue growth, broader market supply and cost trends could further affect future returns, so consider several viewpoints before making a decision.

Explore 3 other fair value estimates on Extra Space Storage – why the stock might be worth just $155.00!

Build Your Own Extra Space Storage Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

No Opportunity In Extra Space Storage?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re here to simplify it.

Discover if Extra Space Storage might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link