")

We Are

Summary

I am positive on Universal Music Group (OTCPK:UMGNF). My summarized thesis is that UMGNF can grow at high-single-digit for the foreseeable future, driven by strong secular tailwinds within the music industry and supported by strong competitive advantages.

Company Overview

UMGNF is a musical label company that operates in three business segments: recorded music (RM), music publishing (MP), and merchandising. In the RM segment, UMGNF basically discovers and develops artists and promotes their music across various formats and platforms. In the MP segment, UMGNF publishes, discovers, and develops songwriters and owns and administers the copyright for musical compositions used in various end media like TV, radio, advertisements, etc. As for the merchandising segment, it produces and sells artist-branded and other branded products. A key competitor to UMGNF is Warner Music Group (WMG), which I have written about here.

UMG

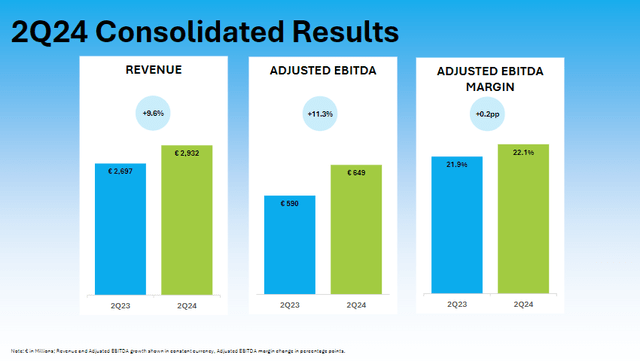

In the latest results (2Q24) reported a day ago, UMGNF reported organic growth of 9.6%, driven by subscription revenue growth of 7%, recorded growth of 7%, publishing growth of 10%, and merchandise growth of 44%. The offsetting segment was a 4% decline in ad-supported revenues. Adj EBITDA came in at 22.1%, missing consensus estimates by 30 bps, but still represented margin expansion vs. 2Q23.

Solid Growth Momentum

UMGNF reported a really solid growth performance for 2Q24 that supports my bullish view on how large music label companies are poised to continue growing over the long term. As I have noted in my post regarding WMG, the music industry has structurally changed for the better as streaming has replaced legacy channels (physical CDs, radio, etc.), which has a long growth runway ahead driven by growing internet penetration globally and an increasing mix of streaming subscriptions within the smartphone user base.

Currently, there are over 700 million music streaming subscribers, which is about 14% of total smartphones (this is a 300bps improvement since 2021, according to IFPI). While it is true that 100% penetration is not plausible, if we use the US as the benchmark, which has ~82.1 million paid subscribers and ~300 million smartphone users, this implies a penetration rate of ~27%, which is close to a double of the global level of 14%. This suggests massive room to grow ahead for WMG. By Eleceed Capital

Mentioned in the 2Q24 earnings call: We’ve identified an addressable market of over 180 million consumers that will form the next wave of subscription adoption and that research is conducted assuming price increases.

I believe the main beneficiaries of this growth tailwind are the big music label companies like UMGNF and WMG because of the structural competitive advantage they have against subscale players. Like WMG, UMGNF has similar competitive advantages, such as:

- Scale advantage, which allows it to deploy significantly more resources to discover and develop artists via better training, promotional activities, etc. And I would think that UMGNF would know how to better identify relevant, promising artists that fit into today’s consumers’ music preferences because it has tons of data to analyze and garner insights from. Importantly, UMGNF is able to take more risk to invest in a large group of new artists, which increases the probability of success (you can think of this like how a VC invests in a portfolio of companies).

- Distribution advantage, which is a big lure for artists because they know that their music will have the widest possible reach relative to an independent label company that probably only has a local reach. The relationship built with various channels and platforms also forms a high barrier to entry for subscale labels because these end distribution partners would prefer to work with UMGNF since they want access to popular music content, which is very likely going to come from huge label companies like UMGNF and WMG.

As such, so long as the industry is growing well (which it is), UMGNF will see a direct positive impact because of its size. The 2Q24 result was very supportive of this, as organic growth continued to stay at ~10%, which is amazing considering that consumer spending is soft and discretionary spending is heavily impacted. One aspect of the 2Q24 results that might have caused some concern is the decline in ad support revenue (down 4%). I strongly advise against inferring this softness as a structural weakness of the UMGNF business. Firstly, remember that revenue is driven by ads, and the advertising market has been soft recently, as evident from YouTube’s ad growth slowing from 21% in 1Q24 to 13% in 2Q24. Secondly, Meta has shut down its premium music videos (PMVs) offering for creators, so that has had some lingering impact this quarter. Lastly, the dispute with TikTok was also a one-off headwind in the quarter.

That said, I believe ad support revenue will recover. Regarding advertising growth, this should trend back upwards as the macroeconomic situation gets better. Digital advertising is still capturing share from offline channels, and with potentially more streaming subscribers, I expect brands to continue allocating marketing budgets to capture consumers’ attention. As for the meta situation, while the PMV deal is off the table, management did note that they are working on another product that involves music content, so this should help in rejuvenating growth. Lastly, UMGNF and TikTok are now partners again after striking a new deal, so that portion of revenue loss should recover in 3Q24.

One reference point is that it was noted that, excluding points 2 and 3, ad support revenue actually grew in 2Q24. As such, I don’t see any major weakness to be concerned about.

Mentioned in the 2Q24 earnings call: Excluding this impact, as well as a lost month of TikTok revenue in the quarter while we were out of license with them, ad-supported streaming revenue grew year over year.

Valuation

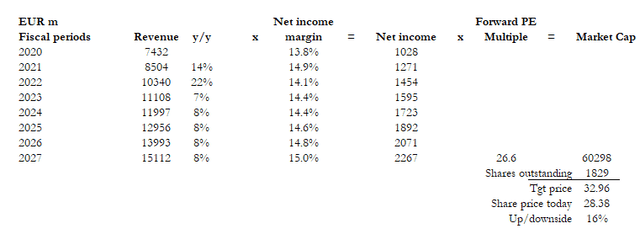

Author’s Calculation

I believe UMGNF is worth more than the current share price. My target price is based on FY27 ~EUR2.3 billion and a forward PE multiple of 26.6x.

Earnings bridge: I don’t see any structural reasons why UMGNF growth will taper in the near term, as the growth tailwind is pretty strong, supported by strong competitive advantages. As such, I model growth to be similar to the industry rate of 8% through my forecast period. I am not incorporating margin expansion, and with this, net income should reach ~EUR2.3 billion in FY27.

Valuation justification: Both WMG and UMGNF traded in line with each other, and the gap has widened to ~28x (OTCPK:UMGNF) vs. 24.5x (WMG). Either UMGNF is overvalued or WMG is undervalued, but for my model, I assume UMGNF is probably trading slightly higher than it should (the historical average is ~26.6x). Assuming UMGNF trades down to 26.6x, I got a share price upside of 16%. The total return is probably >20% if we include the dividends for 2H24, FY25, and FY26.

Investment Risk

UMGNF subscription revenue growth slowed to 6.9% from 12.5%. The risk is that growth may slow down even more in the near term as UMGNF lags last year’s price increases. This may cause the market to be concerned about near-term growth, and hence, valuation may get pressured. My view is that this is just a short-term timing issue; over the long term, the growth outlook is not impacted.

Conclusion

My positivity on UMGNF is because of the strong, robust industry tailwinds and the company’s competitive position. Recent financial performance reinforces my view that UMGNF can capitalize on the growing music streaming market. UMGNF’s scale and distribution advantages position it as a dominant player in the industry. While short-term headwinds such as ad revenue softness exist, these challenges are likely transitory.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

link