")

AzmanL/E+ via Getty Images

Summary

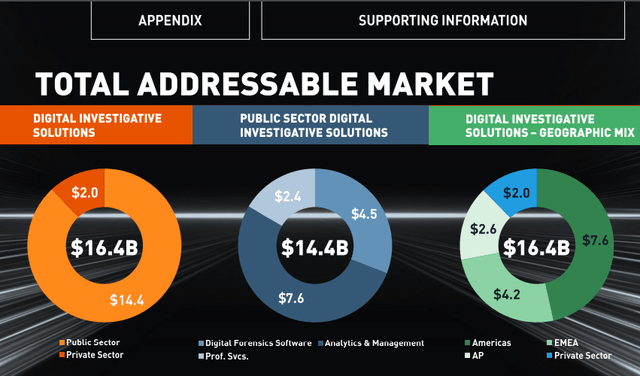

I am positive for Cellebrite (NASDAQ:CLBT). My summarized thesis is that CLBT has a very strong competitive advantage—as the gold standard in the industry—which I don’t see how a new player or other competitor can replicate or displace in the foreseeable future. CLBT serves a mission-critical function, and given the TAM and growth execution so far, I believe a 20% growth rate moving forward is very possible.

Company overview

CLBT is a digital forensics intelligence platform that offers solutions designed to help customers in their legally sanctioned investigations. Targeted customers include law enforcement agencies, governments, and private sector clients. In terms of revenue mix, the majority of revenue comes from subscriptions (86% of FY23 revenue), with the rest coming from perpetual licenses and other revenue (4%), and professional services revenue (10%).

CLBT is the golden standard

CLBT CLBT

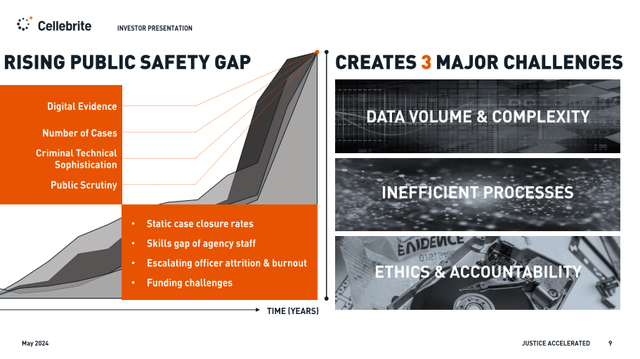

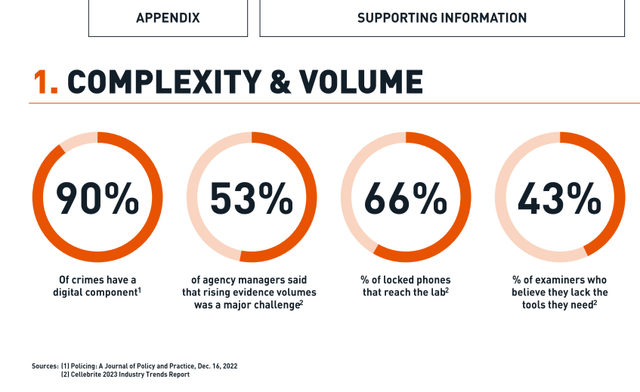

To give a better idea of what CLBT does, they are experts in digital forensics for mobile phones and other devices. They help investigators decipher encrypted data and metadata, including photos, text messages, GPS signals, and WiFi networks that were accessed. In today’s digital world, CLBT solutions are indispensable to digital investigations and evidence gathering for law enforcement. As mobile phones and other digital devices become more integrated into people’s daily lives, so does the prevalence of crime involving them. According to estimates, ~90% of crimes now have a major digital component. What this means is that crucial evidence, which was formerly mostly found in physical objects, is now hidden away in digital devices. By using CLBT, law enforcement can crack encryption on seized devices, retrieve crucial evidence, and analyze it within a short period of time.

CLBT

CLBT’s biggest competitive advantage (barrier to entry) is that it has become widely recognized as the gold standard in the industry. With this advantage, CLBT should be able to continue growing without much competitive pressure. There are two key factors that a competitor must achieve because it can become the gold standard. One is that the product must work without problems. Since this is more of a technical problem, it could be replicated by a team of very smart software developers.

What cannot be replicated is the second factor: adoption by the majority of large, reputable entities. CLBT is currently being adopted by over 6,000 customers, including over 100 North American federal accounts and over 3,000 US state and local accounts in all 50 states. Note that this also includes all the top 20 largest police departments. The importance of having this world-class customer base is that it convinces everyone else (who are not CLBT customers today) that CLBT products work, since they are trusted by these reputable entities (especially those government entities). Notably, once CLBT wins these customers over, they are very unlikely to adopt a new solution provider (it doesn’t make sense to have two when CLBT works well enough), which means competitors cannot replicate this quality of customer base easily.

This competitive advantage snowballs over time because as CLBT wins more logos, their status as the golden standard gets solidified, and this puts CLBT in a much stronger position to win more logos. There are also very few incentives for entities to switch solution providers. Do not forget that these entities are dealing with a person’s life here (criminal investigation), so they are typically more risk-averse and trust something that has worked well (and also what other entities trust) than a new solution that lacks a good track record.

Up/cross selling is a growth driver ahead

FBI

(Source)

The path to growing earnings is not limited to CLBT acquiring new logos. I believe a big part of earnings growth will gradually come from upselling more modules and penetrating adjacent functions. Since FY21, CLBT has sustained net dollar retention at 125% and above consistently, which suggests that entities are adopting more of CLBT solutions (the new logos ARR expansion only contributed 2% of 1Q24 net dollar retention for reference). CLBT has also shown successful execution in penetrating other functions by entering the investigative functions through Inseyets.

Mentioned in the 1Q24 earnings call: And there is also the investigative units, we are augmenting our continued growth in the digital forensic units by accelerating our business in the investigative units of our customers, maybe more specifically that digital evidence captured by Inseyets, open up cross sell and upsell opportunities for evidence management and analytic solutions.

Now, as we advance these initiatives to capitalize to our upgrade, upsell and cross sell opportunities within our installed public sector customer base, we will see our technology deployed more pervasively as we extend our reach into new units, new departments and new buying centers, what we consider to be new sub-logos within the logos we’ve already captured.

Specifically, on Inseyets, CLBT should see more upsell opportunities as it is currently upgrading the majority of its ~32,000 installed base of public and private digital forensic software licenses to Inseyets over the next three years. Execution has been sound so far in 1Q24, and management is expecting 2H24 and 2025 acceleration. Notably, adoption of Inseyets gives CLBT more pricing power as it provides a better value proposition, which management expects to see a 20 to 25% uplift.

Mentioned in the 1Q24 earnings call: The Inseyets may be to deliver considerably more value than the legacy offering. And the higher value obviously enable us, I would say command and enable us higher price tag. That is approximately 20% to 25% higher than the comparable legacy solutions. And we expect that the upgrading the vast majority of the installed base of Inseyets will be completed within the next three years

Valuation

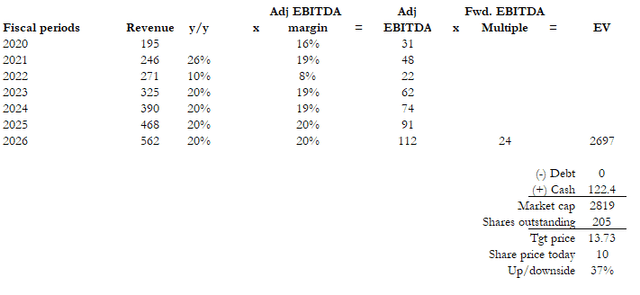

CLBT CLBT Source: Author’s calculation

I believe CLBT is worth 37% more than the current share price. My target price is based on FY26 adj. EBITDA of $112 million and forward EBITDA multiple of 24x.

Earnings bridge: Given the size of the TAM, how much CLBT is as a percentage of the overall budget, and how well CLBT has executed on upselling, I believe a 20% growth rate is a reasonable assumption to make (previous growth CAGR was 25%, and 1Q24 grew 26%). As CLBT scales, I assume the margin will expand accordingly. Using a very modest assumption of 100bps over 3 years (which I don’t think is excessive given that gross margin is at 85% and 1Q24 adj EBITDA margin is already at 19.7%),.

Valuation justification: I don’t see much upside to CLBT multiples, as it is already trading at its historical average of 24x. Multiples could go above this level if growth sustains at 25% (similar to 1Q24), but I don’t think we need to make such an aggressive assumption to get attractive upsides.

Investment Risk

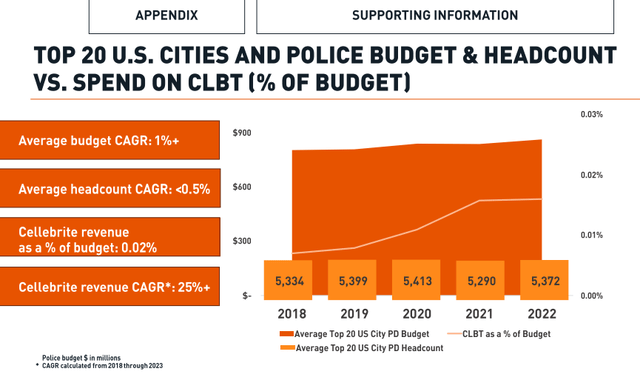

In the government agency and police force segments of the market, CLBT already has a presence with >90% of the relevant customers. The risk to that is that if expansion and penetration opportunities are not as big as expected, the growth could slow as the company has already penetrated the vast majority of those customers (more pressure on upselling).

CLBT products are used heavily in criminal investigations at levels from local to federal. If something occurs that casts doubt on the efficacy or admissibility of evidence from the use of the solutions, that would likely negatively impact sales.

Conclusion

My positive view on CLBT is because of its strong competitive advantage. As the gold standard in the industry, CLBT is trusted by leading law enforcement agencies. This competitive position creates a high barrier to entry for competitors, and this advantage snowballs as CLBT wins more logos and grows over time. The size of the TAM and how much CLBT occupies as a percentage of customer budget also suggest plenty of room for CLBT to upsell existing customers.

link