")

Hinterhaus Productions/DigitalVision via Getty Images

Investment Thesis

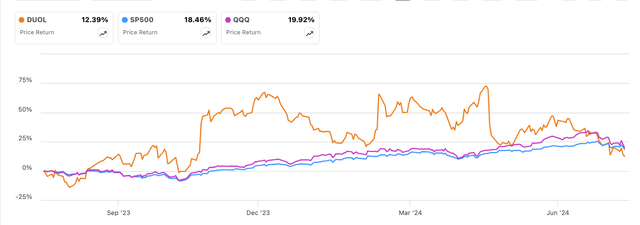

Last year, Duolingo’s (NASDAQ:DUOL) stock outperformed the market and had a decent run. However, it has recently had a slight decline, falling 42% from its peak of $251.

Stock performance (Seeking Alpha)

Not-so-good news has been hitting the market lately. The unexpected increase in U.S. unemployment, the Bank of Japan’s sudden boost in interest rates, and even Warren Buffett’s sale of some Apple shares have all caused investors to get uneasy.

Early in August, a sell-off was triggered by all of this terrible news. To be honest, though, I am a little excited. It is common to find some jewels when everyone is selling. And Duolingo seems like it could be one of them.

Duolingo’s Potential for Growth

It has excellent products and a strong team, which, I think, will help it in the long run. As of present, their share of the language learning market is less than 1%. Even though the economy appears to be in some doubt, I think they have plenty of room to continue rising. For this reason, I have no hesitation about expanding my portfolio at present prices.

What is Duolingo

Duolingo is a popular app for learning languages. It’s free to use, but users can pay for extra features. The company makes money from subscriptions, ads, and language tests.

Competitive Advantage

Many investors believe that Duolingo’s popularity is solely due to its gamified experience. Thus, these investors are concerned that it may not have a moat. However, the tale is not over yet.

When Duolingo first launched in 2011, its mission was to provide everyone with access to language learning education. Because of this, you can use it without charge, although you can pay to remove the advertisements.

Comparison With Spotify

It’s similar to the strategy used by Spotify (SPOT). At first, a lot of people didn’t think Spotify could rival YouTube Music and Apple Music. Spotify does, however, disprove the doubters. Even during the difficult competitive environment, it has continued to grow. Therefore, Spotify’s stock has recently reached all-time highs.

I believe Duolingo and Spotify are alike. While both provide free versions to users, the majority of their revenues are generated by paid memberships. It accounts for 76% of Duolingo’s revenue and 86% of Spotify’s. This indicates to me that customers find significant value in Duolingo’s offerings.

Spotify revenues breakdown (SPOT)

Duolingo revenues breakdown (DUOL)

Not Just Mobile Games

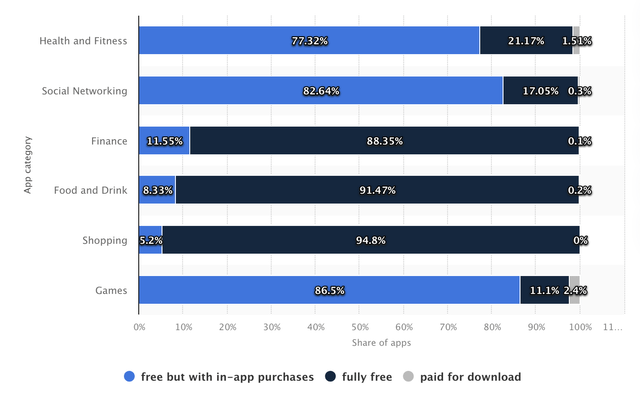

86% (see below chart) of mobile games have a freemium business model that primarily relies on in-app purchases and advertisements.

business model breakdown (Statista)

Duolingo, on the other hand, only got 13% of its revenue from ads and in-app purchases in the first quarter of 2024. That’s a huge difference, and it shows that Duolingo isn’t just another game app.

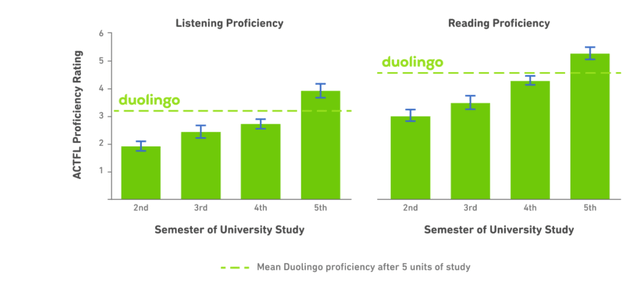

Efficient Learning

Duolingo claims it can speed up the learning process, and they have some pretty impressive numbers to back it up. Their users are reaching a 4-semester university language level in about 120 hours. That’s half the time it’d take in traditional university classes. It’s quite an achievement.

Efficiency comparison (DUOL)

Academic Recognition

The Duolingo English Test is now accepted by top colleges, including Ivy League schools like Harvard and UC Berkeley. This makes Duolingo a certified player in the language learning field and differentiates it from many of its competitors.

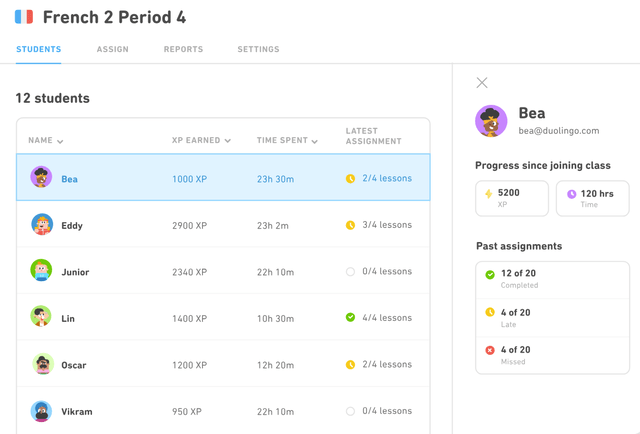

Classroom Integration

Another interesting point: teachers love Duolingo for Schools. It tracks student progress, giving detailed insights on accuracy and time spent learning outside the classroom. It’s saving teachers time and becoming a go-to tool for personalized education management. As Duolingo branches out into math and music, these tools could shake up the traditional education system.

Duolingo for School (DUOL)

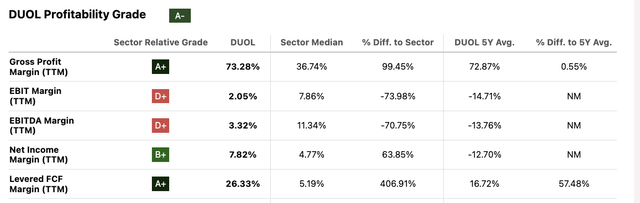

Therefore, Duolingo’s subscription model is built on real value, not just fun and games. That’s giving them a solid edge in the market, with margins that are already impressive compared to their peers.

Margin comparison (Seeking Alpha)

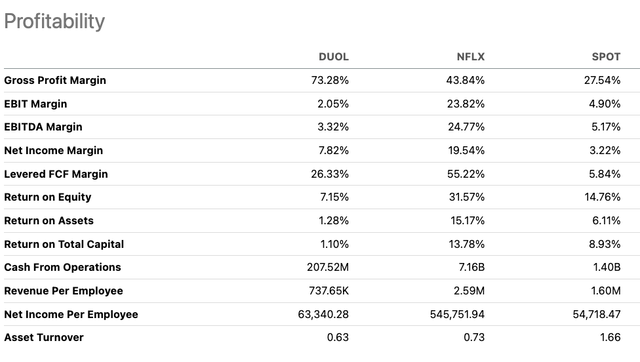

Stacking Up Against Other Subscription Services

Netflix (NFLX) and Spotify are two examples of profitable subscription businesses. Another way to look at Duolingo’s competitiveness is to compare the profitability of the various subscription plans.

Duolingo’s premium revenue per user is $96 (calculated from financial reports), which beats Spotify. Netflix’s number is higher, but they don’t break out their ad revenue, so it’s not a perfect comparison. I crunched the numbers and figured out Duolingo’s total revenue per user is about $126 – not far off from Netflix. It’s pretty competitive.

Comparison (From DUOL, SPOT and NFLX and edited by author)

What’s impressive is Duolingo’s margins. They’re doing exceptionally well compared to Netflix and Spotify, both in gross margin and free cash flow.

Margin comparison (Seeking Alpha)

My take is Duolingo is spending way less on content and thus has a higher gross margin.

App Store Rankings

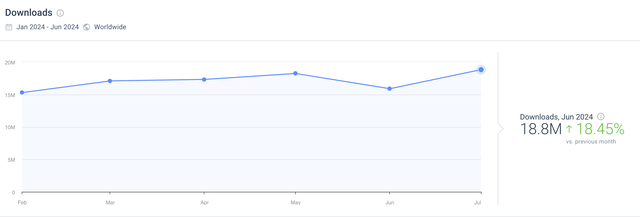

According to SimilarWeb (see below chart), Duolingo’s topping the charts in downloads for education apps in a bunch of countries, including the US, China, and Russia. Their downloads jumped 18% last month and have been trending up for the past couple of months.

Download trend (SimiarWeb)

Download ranking by countries (SimiarWeb)

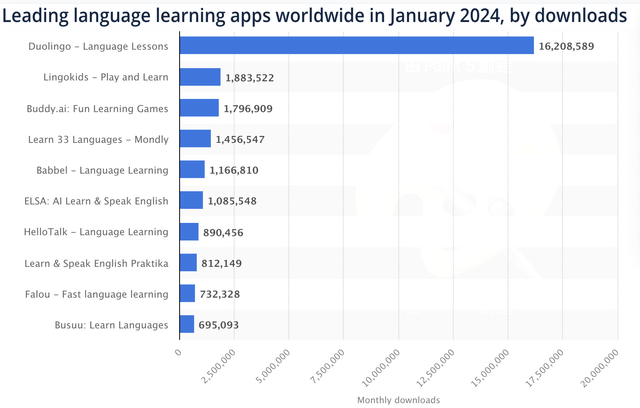

Statista’s data (see below chart) shows Duolingo’s download count is 10 times higher than their closest competitor in education for 2024. That’s a pretty commanding lead.

Download ranking (Statista)

Valuation

Market Projections

Management projected the language learning market to hit $115 billion by 2025, growing at about 11% a year. Right now, Duolingo’s got a tiny 0.46% (calculated from its financials) slice of that pie. The online part of the market is expected to grow even faster, at 26% a year, reaching $47 billion.

Management mentioned that most of the language learning market is focused on English, but less than half of Duolingo’s users are learning English. That spells opportunity to me.

Duolingo user breakdown (DUOL)

So, here’s my thinking: if Duolingo can grow to just 1% market share in 10 years, we’re looking at $5.7 billion in revenue. That’s a 27% growth rate year over year.

Duolingo MAXThey’re also rolling out Duolingo MAX, a pricier subscription. Management’s still figuring out the best pricing, so they haven’t pushed it to everyone yet. They think it’ll be more profitable than its current plan. Theoretically, this new product offering can increase its margin long term, but I’m playing it safe in my calculations. I assume it will maintain its current 27% free cash flow margin long term.

Using a beta of 0.72, I estimated the stock’s WACC at 8.8%. Putting it all together, I value the company at $15.4 billion. That’s a 97% upside from where we are now.

DCF (Author)

The Risk Factor

Competition

There’s a new entry on the block worth keeping an eye on: Speak. This startup’s grown to 10 million users since 2019. It just got back from OpenAI, doubling its valuation to half a billion dollars.

Speak charges $20 a month or $99 a year for full access to its features, including review materials and special courses.

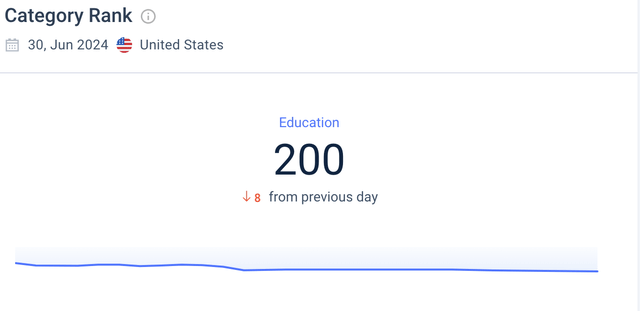

According to SimilarWeb (see below chart), Speak is currently ranked 200th in US education app downloads. Its ranking’s been slipping, but this company is still one to watch.

Spark’s download ranking (SimilarWeb)

Speak’s using AI for products like roleplaying, similar to Duolingo MAX. The competition in AI language learning isn’t fierce yet, but it’s growing. Duolingo is using ChatGPT rather than developing its own AI model, which might make it harder for it to stand out in this area. If AI becomes the main draw for language learners down the line, Duolingo might lose some of its edge.

Final Thoughts

I think education could be a smart bet for investors when consumer spending is tight. There aren’t any big tech giants dominating this space yet. Duolingo’s got a ton of room to grow, given its tiny market share and solid product. So, I am looking to buy more when the market is in a selling mood.

link